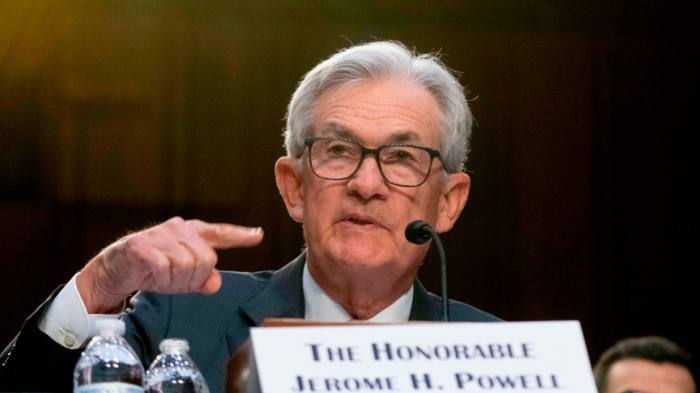

Fed chair Jay Powell struck a hawkish tone in front of the Senate banking committee on Tuesday.

Recent economic data was “stronger than expected” he said and

“the ultimate level of interest rates is likely to be higher than previously anticipated”.

Two sets of data – the monthly jobs report due on Friday and last month’s CPI report due next week – will be released before policymakers next meet. Both will be essential in determining the Fed’s next move, with

experts saying its reputation is at stake.

“If demand continues to reaccelerate, this will most likely be met with higher interest rates,” argues Karen Ward, chief market strategist for Europe, Middle East and Africa at JPMorgan Asset Management. “For now,

both stock and bond investors should expect good economic news to be bad news for markets,” she warns.

Powell’s sentiment echoed that of Christine Lagarde, president of the ECB, who warned that price pressures were “sticky”. But Andrew Bailey, governor of the BoE, took a different path, treading very carefully around rate rises last week.

More recently, an external member of the BoE’s monetary policy committee, Swati Dhingra, argued that

UK central bankers should keep rates at 4 per cent. “In my view, a prudent strategy would hold policy steady amid growing signs external price pressures are easing,” she said. “... This would avoid overtightening.”

Clouds darken over the City of London

Last week CRH, the world’s largest building materials group, announced it would shift its listing from London to New York. SoftBank also shunned listing Cambridge-based chip designer Arm in London in favour of New York.

Sources said that Arm was deterred from listing in London because of a rule that requires UK plcs to disclose all related-party transactions, alongside cost and complexity of the process. This led some UK officials and SoftBank insiders to

blame the FCA for the decision.

But that seems churlish, argues business columnist Helen Thomas. The regulator is already reviewing premium requirements and initial findings last year showed “most respondents saw value in the related party safeguards and few cited them as a barrier to listings”.

She points to “long-term pensions reform, rebuilding a dwindling domestic investor base, and closing a valuation discount born in part out of Brexit and political dysfunction” as factors that also need to be addressed.

The

chief executive of the London Stock Exchange Group, David Schwimmer, was unperturbed. In reference to CRH’s news, he said: “If companies are going to make decisions when most of their business is in the US, that sort of is what it is.”

Others are concerned about the future of the LSE. “We’ve been in perpetual drift,” said Sir Nigel Wilson, chief executive of Legal & General. “There’s a drift of the City to Europe, there is a drift of the City to the United States.”

The UK is a “low-productivity, low-growth, low-wage economy fraught by political infighting,” according to Wilson, who also noted the shift from equities to bonds by UK pension funds as part of the reason London was struggling.

Indeed, Richard Buxton, UK equity fund manager at Jupiter, and David Cumming, head of UK equities at Newton Investment Management, have both called for a

change in pension accounting rules to boost domestic equity investors and demand for London-listed stocks.

Business investment and tax regimes

There’s a double threat on the horizon for British businesses – the end of the “super-deduction” tax break for investment and a 6 percentage point hike in corporation tax.

Companies will be looking for some good news in next week’s Budget, with business groups expecting

Chancellor Jeremy Hunt to set out modest reforms to capital allowances.

Meanwhile in the US, oil companies have spotted an opportunity to make the most of the subsidies in the Inflation Reduction Act.

The law incentivises investment in some lower-carbon technology and fuels, so oil

companies are starting to fund projects such as carbon capture and storage, refitting refineries to make biofuels and hydrogen production – all helped with IRA subsidies.

“This is not a game for start-ups,” ExxonMobil chief executive Darren Woods told investors. “These are large, world-scale projects that require the kind of project expertise that we have, require the kind of size and balance sheet capacity that we have.”

But there is one hitch in the IRA breaks for multinationals –

the global minimum corporate tax. The 15 per cent rate was agreed by 130 countries in 2021, but it’s unclear how this OECD deal will work with the US’s green energy tax credits.

The worry is that the IRA’s tax credits could reduce a company’s tax liability in the US to under 15 per cent. This means multinationals who are investing in the US are at risk of being taxed by foreign governments under the “top-up” mechanism.

That’s not just a problem for business – it could also mean a “massive US tax transfer to foreign countries”.

Workplace culture and the changing role of directors

Workplace culture has been front and centre of recent headlines. This week it was announced CBI director-general Tony Danker has decided to step aside

while an independent investigation is under way into his workplace conduct.

Last week in Germany, N26’s chief risk officer Thomas Grosse resigned. The company said this was due to personal reasons, but Grosse is the

third senior executive to leave in less than 12 months.

The move raises questions around internal governance: Grosse was in charge of improving N26’s anti-money laundering controls as ordered by the German regulator BaFin.

But

workplace culture at the fintech, which has one of Europe’s highest valuations, has also come under scrutiny. In an internal memo sent in February last year, N26’s six most senior employees, including Grosse, warned co-founders Max Tayenthal and Valentin Stalf that their “relationship and ways of working” with executives were “quite dysfunctional in several dimensions”.

And finally, our Working It podcast

takes on “overboarding”. Investors have voted against directors whom they believe have overcommitted themselves – Egon Durban being one prominent example.

But this nods to a wider trend that the role of a director “has become increasingly complex, increasingly demanding and increasingly transparent”, says corporate governance expert Patricia Lenkov.